The first time I was approved for a mortgage, I was looking for a home around $200,000 based on my income and bills. A mortgage around there would have made things comfortable.

I was approved by my lender for a mortgage up to $350,000.

“What was that?” was exactly my reaction. Knowing my budget, I knew I couldn’t afford anywhere near $350,000 and still be able to eat (I like to eat).

Yet they approved me for that much—and this was in 2012 after the housing bubble burst!

The reason for that is because lenders look at only your current liabilities and income. They don’t look at how much your grocery bill is or how many subscription services you have.

They don’t look at your utility bills or your $200 monthly train ticket so you can get to work.

That’s why more than ever, it’s up to you to determine how much you can afford.

So let’s dive into what happens when you start thinking about buying a house. Then, we’ll get into exactly how you can determine how much home you can really afford to buy.

The Pre-Approval Process

The first thing you’ll want to do when looking for a home is to get pre-approved for a mortgage.

Not only will you know how much money a bank is willing to lend you, but it also gives you an advantage when putting offers in on a home.

Home sellers look at a lot of things when considering whether to sell to a potential buyer.

Pre-approval letters state that everything looks good and that there’s a good chance the bank will loan you money.

This can put the seller at ease and gives you an automatic advantage over offers that choose not to get pre-approved.

So what do lenders use to determine your eligibility?

Lenders Look at Credit Score and History

When applying for a mortgage, your lender will pull your credit score and history with what is called a “hard inquiry.”

A hard inquiry can affect your credit score and stay on your credit report for up to two years.

Generally speaking, the higher your credit score, the better the chance you’ll get approved for a loan.

Even beyond just getting approved, your credit score will help determine your interest rate.

If you have a lower credit score, lenders will see you as a higher risk. That means your interest rate will be higher to offset this potential risk to the lender.

The exact opposite is true of a higher score. If you have a higher score, the lender sees you as a lower risk and can offer you a lower interest rate.

Lenders Look at Debt to Income Ratio

As part of your credit check, the lender will also have access to all of your other debt as well. They will also ask for pay stubs and W2s so they can look at your monthly income.

Lenders will compare your income to your debt in what they call “Debt to Income Ratio.”

Basically, they’re just determining how much of your income is already going toward debt.

This helps them decide if you would be able to afford a monthly mortgage payment to eventually pay off the loan.

Banks will also use this information to determine exactly how much of a mortgage payment they think you can afford.

If you have a good credit score, the likelihood of getting approved may be high. However, if you have a ton of credit card debt, the lender may not approve you for as much as you need for a house.

In most cases, if you’ve been at your current job for a while, they’ll ask for your most recent two pay stubs. If you have recently changed jobs, they will ask you for more pay stubs and possibly stubs from your last job.

Lenders Look at Job Stability

Similarly, banks also look at your income to determine job stability.

If you’ve been employed for quite some time, it looks better on your mortgage application than if you went through a period of unemployment, even if it was by choice.

Just like with debt to income ratio and your credit history, banks will look at your job stability in order to determine the risk of loaning you the money for your house.

Lenders will usually ask for your W2 forms for the past two years. This is a sufficient amount of time for them to determine that you’re a lower risk.

If you’re self-employed, it will probably be a little harder to obtain a mortgage. You’ll not only need to provide your bank statements and income for the past two years, but you’ll need to prove that you have steady work currently.

You’ll also want to be doubly sure your credit history is good given that your job stability may look a little shaky to banks as self-employed.

Lenders Look at Bank Account and Asset Information

Lenders will ask for your current bank statements as well as the most recent previous month as well. They want to see what is currently in your bank account.

They’ll also ask for any asset information such as a 401K or Roth IRA account. Basically, they’re looking for any money that you’d be able to use to pay off the loan, even if you don’t want to use it.

If you have a downpayment, your bank account will also prove that it’s yours or a gift and not a loan that you have to pay back.

Your Pre-Approved Amount Will Be Too High

After looking at all the stuff above plus some additional minor things (like your license), the bank will make its decision. If you are approved for the mortgage, they’ll give you a total dollar amount that they will lend you.

This dollar amount is usually way higher than you may be able to afford.

Remember my experience and getting approved for $350,000? There is literally no way I would have been able to make that payment on the income my wife and I were making then.

Again, banks don’t look at the whole financial picture through all of this. They won’t ask you for all of the bills you pay every month.

Here’s what you’ll want to do to determine how much you can afford?

Step 1: Get Your Budget in Order

Budgeting is the foundation of all other areas of personal finance—the root system of your financial tree. The same is true in this situation.

I can’t stress enough how important having a handle on your budget is to this process. It allows you to see how much money you’d feel comfortable spending on a mortgage every month.

Your first step will be to make sure that you know what’s going on in your budget so you know how much money you have every month.

Compare your current income to your current bills and see how much wiggle room you have with your current house or rent payment.

Would you feel comfortable with a higher payment or do you have to have one around the same amount you have now?

Don’t just look at dollar amounts either. Look at the things in your budget that you like to do.

Will you have to cut out some things you value to afford a higher payment? If yes, are you ok with doing that in the short(ish) term?

Look at the big picture of your budget, determine what sort of payment you can afford based on that, and then move on to step two.

Step 2: Check Your Credit Score

I’ve recently explored CreditSesame. They are an online website that allows you to check your credit score for free.

It’ll also grade you on a few other key metrics like:

- Payment history

- Credit usage

- Credit age

- Account mix

- Credit inquiries

The number of emails I initially got from them was way over the top (glad there’s an unsubscribe button), but I really like their tool.

You can use CreditSesame to get a good picture of your credit score. You also may have a credit card that offers this service already without the bells and whistles.

Your credit score has a big impact on two areas of obtaining a mortgage—the chances of you getting approved, and more importantly, how high your interest rate might be.

If you have a good credit score—700 or above—you can expect a good interest rate. If your score is a little lower than that, you may still get the loan, but your interest rate may be higher.

Find out your credit score, and then move on to step three.

Step 3: Look Up Interest Rates

Unlike credit cards or car loans, I’ve never heard of a 0% introductory or permanent interest rate on a mortgage. If you have, let me know. I’ll get my closing documents ready.

This means that an interest rate is a big part of a mortgage.

Look up the average interest rate for your credit score. A google search such as “current mortgage rate for good credit” should work for you. You can even include your state name in the search to narrow it down.

The goal is to find an average of what your interest rate might be so you can budget for it.

The average interest rate when I applied a few months ago was 4.5% for a 30 year fixed mortgage. I used that amount to see if I could afford the house we wanted.

Shopping around and getting a 4.25% interest rate instead was just icing on the cake since I already knew I could afford a 4.5% interest rate.

When looking for interest rates, consider how long you want to have the loan. Most people choose a 30-year fixed mortgage, which means it is amortized over a 30-year period at a fixed interest rate.

You can also choose a 15-year fixed mortgage. 15-year loans often have lower interest rates because the bank is considered less at risk since the term of the loan is shorter.

A 15-year mortgage will also significantly cut the total amount of interest you pay since the loan is shorter.

I chose a 30-year fixed mortgage. Choose what works best for you and then keep that in mind when looking up interest rates.

Write down what the average interest rate of a mortgage would likely be for you and then move on to step four!

Step 4: Consider Your Downpayment

One of the big things to consider when applying for a mortgage is how much your downpayment is going to be.

Obviously, the bigger the down payment you have, the less your monthly payment will be. However, your downpayment amount affects more than just your monthly payment.

If you have a lower income or lower credit score, many lenders may not even consider you for a mortgage unless you have 20% of the mortgage amount to put down.

That’s where FHA loans come in. FHA loans are government-insured where you only need to put 3% of the total mortgage amount down.

In almost all cases, a down payment of less than 20% requires mortgage insurances, whether it’s Private Mortgage Insurance (PMI) or the government-insured variety of the FHA loan.

Consider how much money you have to put down, and if you’ll have to pay PMI, and factor that into how much house you can afford.

Write down your down payment in the same place as the interest rate you’re going to use for your estimated payment.

Onward to step five!

Step 5: Look Up Property Taxes in the Area You’re Looking

Property taxes are usually factored right into your mortgage payment in what is called an escrow account.

An escrow account simply holds the money that is used to pay your property taxes and homeowners insurance and is usually associated with the lender you choose.

Property taxes are a huge part of your monthly payment.

To give you an idea, what would be considered my actual mortgage payment on my $290,000 mortgage is only $1,141.30. Not a terrible amount of money.

However, I also need to put $591.10 every month into my escrow account to pay for my property taxes and homeowners insurance bringing my total payment to more than $1700 dollars a month!

Property taxes alone are $518.18 a month and I have to pay them if I want to keep my house. Essentially, it’s not just your mortgage payment you need to be able to afford.

Look up the average property taxes for the area where you’re looking to purchase a home.

Redfin and Zillow will have this as part of their listings, although I’ve found that it isn’t completely accurate. If you go this route, I recommend overestimating a little bit.

You can also go straight to your County Assessor’s Office since property taxes are considered public record. You’ll need the complete street address of an example home.

If you’re really into numbers or are just curious about what goes into figuring out property taxes, you can also try and do it on your own. Here’s a great article to help you out with that.

After you figure out an average of the property taxes in your area, write down what you’d be paying yearly, and then move on to step six.

Step 6: Find Your Average Homeowners Insurance Premium

Again, not only is it important to be able to afford your mortgage but also the tax and insurance payments that go with it.

Luckily, homeowners insurance usually isn’t terribly expensive. When you decide to pick a home, I recommend shopping around a few different places for insurance.

If you already have an insurance provider for car insurance, they may give you a discount since you will be adding another policy. They are a good place to start but don’t be afraid to check others.

For now, you’ll want to look up average homeowners insurance policy premiums since an insurance company wouldn’t be able to give you a decent quote without a property.

According to Value Penguin, the average cost of homeowners insurance across the country is $1,083.

My lender gave me an estimate of $960 in my loan disclosure so your mileage may vary.

Remember, it’s better to overestimate your premium rather than underestimate it. That way if it only can go down, you know you’ll be able to afford it.

For simplicity’s sake, you can just make it an even $1200 yearly premium for estimating your payment.

Whatever number you decide, figure out the monthly payment amount based on the yearly premium.

Write the number you’re going to use down with your property tax, down payment, and interest rate numbers, and then it’s time for step seven.

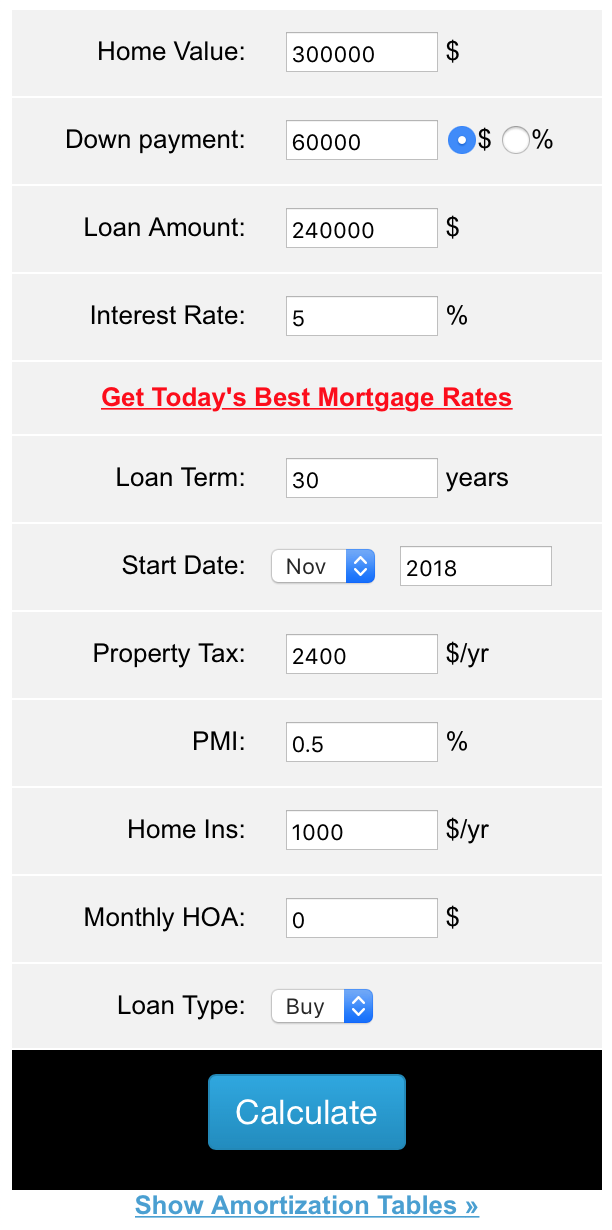

Step 7: Use a Mortgage Calculator

Using a mortgage calculator will show you the exact payment and amortization schedule you can expect to pay on any mortgage amount you put into the calculator. This is a great way to figure out how much payment you can afford.

Before we enter our numbers in, here is what you should have written down to put into the calculator:

- Interest rate – The rate you looked up based on your credit score

- Downpayment – The amount you either have or plan on having to put down on a home

- Average property tax amount – The yearly estimated property tax payment

- Average homeowners insurance premium – The yearly amount you’ll likely pay for insurance

The mortgage calculator I like to use is at https://www.mortgagecalculator.org. Simple and quick, but a quick Google search for a mortgage calculator will bring up other options as well.

Let’s get Calculating!

- Start by putting in a home value. If you’re just starting out you can put in an example number of how much you think you’ll want to purchase. Otherwise, if you are eyeing a few homes already, start putting the sale price amounts into the calculator.

- Put in your estimated downpayment. You can play with this number after your first calculation to see what a difference a higher or lower downpayment can make.

- Enter your average interest rate. This is the number you wrote down based on your research and credit score.

- Select your desired loan term. Again, I’m on a 30- year mortgage. You can select between a 30 or 15-year term if you’d like to see the difference in total interest and monthly payment.

- You can leave the start date where it’s at since we’re only estimating.

- Enter the estimated property tax you have written down. Remember, since the calculator is asking for yearly, we want to put in the yearly amount.

- Enter the PMI amount. If you’re not putting 20% down, you’ll more than likely pay PMI. This is usually anywhere between .5% to 1% of the loan amount on a yearly basis. A $200,000 home at 1% PMI would cost you $2,000 a year or $166.67. If you’re not putting 20% down, put a higher percentage for PMI just so you can set the correct expectations for yourself.

- Put in your yearly homeowner’s insurance estimate. This is based on the research you did in step six and had written down.

- If your desired subdivision does have a Home Owners Association fee, put that in the last field. The number of subdivisions that have an HOA is growing, but it isn’t too big to automatically include it in your estimate. Just something to keep in mind.

Hit the calculate button!

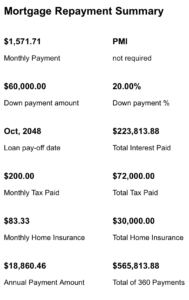

After some hamsters running on a wheel and some really smart people working spreadsheets (just kidding—the site is pretty fast), you’ll be given your payment.

Along with your monthly payment amount, it gives you some other cool numbers like total interest paid over the life of the loan plus your total amount paid for the house after your loan term is up.

Don’t be nervous when you see the total amount you’ve paid over 30 years. My $300,000 example house actually cost me $565,813.88 over the life of the loan.

Unless you’re paying cash for a home, this is just the name of the game and shouldn’t scare you off from owning your own home.

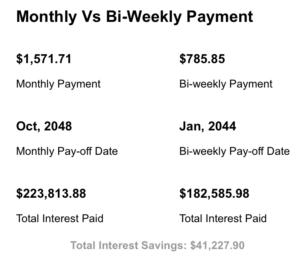

What’s cool about some mortgage calculators like mortgagecalculator.org is that it gives you a breakdown of the difference an extra payment a year can make. It looks like this.

To make biweekly payments, you just split your mortgage in half and pay every two weeks. This works well for people that get paid every two weeks as opposed to monthly or semi-monthly paychecks.

If you’re making biweekly payments, you end up making an extra payment every year. Doing this can save you a ton of money on interest and will pay off your mortgage early.

It’s just something to keep in mind if you want to build that into what you want to afford.

One last step! Onto number eight!

Step 8: Play Around with the Numbers to Get the Payment You Want

After you’ve made your first calculation, you will have a picture of what your mortgage payment might look like.

Compare this number to your budget and see how it looks.

If it’s too much, play around with the numbers in the calculator to get a more affordable mortgage payment.

If it fits too comfortably, decide where you want to put the extra money. You can put it toward more house or toward other goals or things you value.

Figuring out the payment you need can also be used to determine what you would like to pay for homeowners insurance and what interest rate you want to get.

If you have a lower interest rate, you may be able to afford a higher mortgage amount.

This is also true of homeowners insurance. A $1200 yearly premium versus an $800 yearly premium means about a monthly payment difference of a little over $33 a month.

It may not be much but every little bit helps.

Final Thoughts

Just like with a budget, this is all about you. Figure out a payment that will be comfortable for you and then go from there.

Don’t let lenders dictate how much you can afford. If I did that, I’d be living on the streets—or with my mom—because of not being able to afford my house payment.

Use the eight steps above to figure out how much you can afford based on where your life and budget are right now. You’ll be able to adjust your downpayment, potential interest rate, and other areas to give yourself the correct expectation of what you can handle for a monthly payment.

The goal is to be able to enjoy your life while you are enjoying your new home. And only you can know what that looks like.