Budgeting on a variable income can be a beast. There isn’t any normalcy.

You aren’t sure if you’re going to make enough money this week to pay your bills.

Things can feel really uncomfortable trying to budget when you’re not bringing home the same amount every paycheck.

You may have even given up on budgeting because it seems too difficult.

If you’re not getting paid the same amount of money regardless of how many hours you work, I’ve got some hope for you.

Budgeting on an irregular income can be easy, you just have to do it a little differently than you would a normal budget with a salary.

By the end of this article, my goal is to have you feeling very comfortable budgeting on your variable income.

I’ve Been in the Same Boat

I’ve been right where you are before. When my wife and I got married, I was at an hourly restaurant job and she was working for a survey company.

We were making barely $10 an hour each.

Her hours were fairly steady, but mine were not. I worked 30-37 hours every week and there was no telling what end of the spectrum it was going to be.

Budgeting was definitely a challenge with all of the variables. I was young. I didn’t know much about managing a household’s money. The numbers weren’t regular.

I’m squirming in my chair just thinking about it.

So what did I do?

I ignored it. I didn’t think it could get any better so I didn’t try.

We had a $10,000 loan that we took out from my wife’s grandma that we were planning on using for a home, but that’s not where it ended up.

I didn’t think there was hope so we didn’t budget well, overspent on things, and depleted that $10,000 in just a couple of years.

You hear it all the time, but if I knew then what I know now, we would be in a very different place.

We would have been in control a long time ago.

Don’t ignore it like I did!

Nine Things to Do to Budget on an Irregular Income

So how do you budget without a fixed income?

In short, you have to make some tweaks. You don’t have the same amount coming in every paycheck but what you can count on is something coming in every time you get paid.

Let’s work with it so you feel confident in your budget and income.

Here are nine things you should change in your budget if your income isn’t fixed.

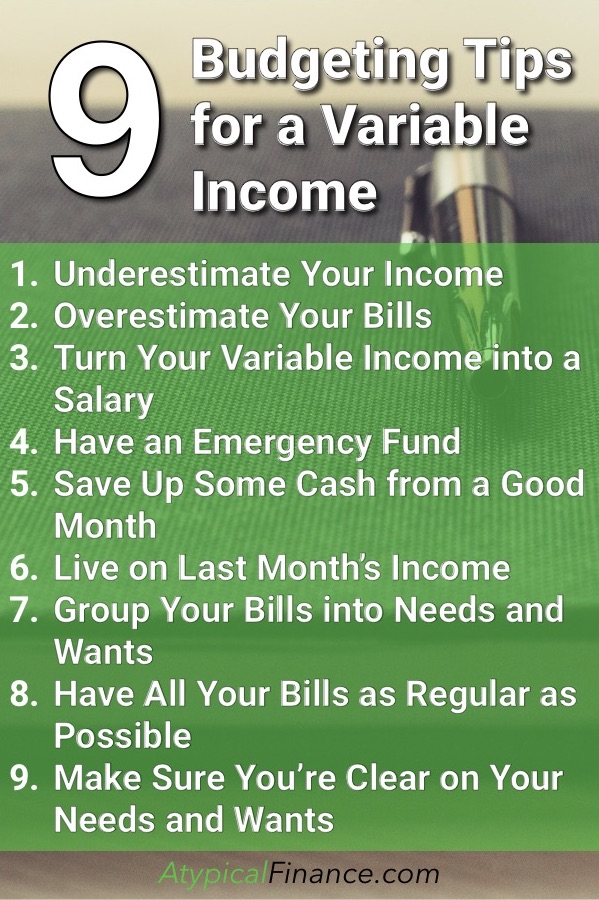

1. Underestimate Your Income

Have you heard the saying “plan for the worst and hope for the best?”

This is the budgeting version of that.

Since you have to estimate your income to budget on an irregular paycheck, you always want to underestimate.

The idea is that even during months where you are a little leaner in the money department, you still have enough to at least cover your bills.

Here’s how to do it.

Take a look at your monthly income over the course of the past year.

Where was it at its lowest?

Does that lowest month cover your current expenses?

If it does—and if you’re confident your checks won’t go below that—use that as your income baseline. As long as you hit that amount you’re good.

If your lowest income month doesn’t cover your expenses, take a look at the next lowest month. Does that one cover it?

If you’re lowest three months of income don’t cover your current expenses, you may be experiencing lifestyle inflation.

It may be a good idea to look at your expenses and see what to cut out so you’re not living every month like it’s a great income month.

If you’re lowest three months cover your current expenses, plan your expenses around that one of those months.

Then if you make more than that, you can use it for debt payoff, saving, or retirement.

Related articles:

2. Overestimate Your Bills

At the same time, if you have bills that are variable, it’s a smart move to overestimate them.

Similar to how underestimating your income gives you some wiggle room, overestimating your bills ensures that your budgeting enough so your bills are always taken care of.

This means things like gas for vehicles, groceries, utility bills—basically anything that depends on you paying for what you’re using should all be overestimated.

Figure out an average of what you spend on them each month, and then add $25 or $50 to that amount.

This gives you some wiggle room in your budget. Then, anything left over at the end of the month can just roll into the next month.

I love a good, fluffy cushion!

3. Turn Your Variable Income into a Salary

3. Turn Your Variable Income into a Salary

3. Turn Your Variable Income into a Salary

3. Turn Your Variable Income into a SalaryTaking the first tip a step further, once you’re at an amount that will consistently meet your expenses, why not automatically put everything above that into savings?

Essentially, what you are doing is turning your variable income into a predictable salary income.

Plan for your set amount just as if you had a salary

Then anything over and above that can be used to reach your financial goals.

Put it towards debt or an emergency fund. Save up for a vacation or home. The sky is the limit with this money.

4. Have an Emergency Fund

Despite our best intentions, things happen.

Cars break. Houses break. Medical issues occur.

All of these things can happen out of nowhere. While it’s important to plan for things like this, having a solid emergency fund to back you up is a must, especially with a variable income.

Now, there is no set amount that I can tell you to put in the bank because your situation is different from mine. In fact, everyone’s situation is different

But I can give you a starting point.

I recommend having at least $1,000 in the bank as an emergency fund. This is a good starting point and will provide at least some sort of safety net if a financial emergency does happen.

Beyond that, it’s up to you how much you want to have. I recommend asking yourself three questions to figure that out.

- How much extra money do you already have per month? Do you generally have months that are leaner or do you have a decent amount extra each month?

- What is the likelihood of you having a financial hardship? Is your job secure? If you’re a salesman or saleswoman, are you in a time of year where it might be a little slower for sales?

- What’s the smallest emergency fund you’d feel comfortable having? This is what matters. Do what is right for YOU and your situation and life.

From there, build your emergency fund up to the number you’ve settled on and then rest easy that you’ve got a safety net in case something falls apart.

Related articles:

Emergency Funds: Why, How Much, and How to Build One Quickly

5. Save Up Some Cash from a Good Month

If you’re having an exceptionally good month for income, you can put that toward your budget for when you have a month where it’s a little bit of a struggle.

Imagine this. You’re a sales rep and you have a really good month. You get paid an extra $500 in commissions.

You take $400 of that extra cash and split it up between your grocery and gas budgets, and then use $100 to celebrate in your eating out budget.

A couple of months down the line you aren’t able to sell as much as even a normal month. You didn’t make quite enough to cover all of your needs, but because you have $200 extra in each of your gas and grocery budgets, you have no problems making ends meet.

In that situation, you’ve used some money you made a couple of months ago to help keep you afloat this month.

And you didn’t even have to dip into your emergency fund!

6. Live on Last Month’s Income

Taking that a step further, you could always live on last month’s income.

The idea is to not have to touch the income you’re earning this month for any of this month’s bills.

The income you made last month will be spent on this month’s bills. This month’s income will be spent on next month’s bills.

Now, that’s a simple explanation but this is easier said than done. The best way I’ve found to do this is to create a buffer in my account. This will be a separate item on your budget.

As you have good months, put away money using this buffer to create some space between your bills and income. When you have enough in that buffer budget to be equivalent to your normal income, you can distribute it to your bills.

Now, you put this month’s income into that buffer category while the income you saved up as a buffer does the work of paying this month’s bills.

Keep this pattern up and you’ll be living off last month’s income every month!

This method is built right into the budgeting app I’ve used for a couple of years now called You Need a Budget. It’s a phenomenal app that has been great for getting control of my money and meeting my financial goals.

7. Group Your Bills into Needs and Wants

This is one of the best things I’ve done for my budget.

I took all of the things that I absolutely need to purchase—food, housing, etc.—and I grouped it all into an overarching “Needs” category.

I did the same thing with wants like eating out, movies, video games, and toys for the kids by putting it into a “Wants” category.

To be clear, I still track each of those subcategories too.

The idea is to be able to make necessary cuts in your budget if you’re having a slow income month.

Instead of sifting through every category that you budget for, you can go straight to your wants knowing that anything in there can be cut out and you’d still be ok. This makes it really easy to cut spending in some areas.

It also gives you a lot of flexibility. You are free to cut out some eating out so you can see the latest movie if your income is a little short.

Alternately, if you want to catch the latest movie on a $5 Tuesday night, you can opt for that instead or you could wait to see it until next month.

The options are endless to give your variable income more flexibility but your needs will still be met.

8. Have All Your Bills as Regular as Possible

Just because you’re dealing with a variable income doesn’t mean everything has to be variable.

It’s a great idea to try and solidify the amount of money going out of your account to take out some of the variables. Here are some ideas:

- For utilities, see if your providers have a program where your bill is the same every month with an adjustment at the end of the year. 11 out of 12 months your bill will be the same amount.

- Stick with services like Netflix or Hulu Plus that are the same amount every month for their service

- For credit cards, as you pay down the balances, your minimum payment starts to diminish. Continue to pay the same amount even if your minimum payment is less

There are a few ideas to get you started. The less volatility you have in your bills, the easier it’ll be to budget for your variable income.

Related: The Best Way To Pay Off Debt With Little (Or NO) Extra Money

9. Make Sure You’re Clear on Your Needs and Wants

Budgeting, in general, is much harder if you aren’t clear on your needs and wants.

That difficulty is only multiplied when budgeting on a variable income.

Cut out the things in your budget that don’t bring you joy.

Things like having a subscription you don’t use, spending on things you give up on after a couple of weeks, and letting your emotions dictate your spending are all some of the things that can sabotage your budgeting efforts.

Don’t be afraid to set aside some time to think and really be honest with yourself about what you spend money on.

At the same time, if something is a need for you, do not be afraid to find a way to include it in your budget regardless of your income that month.

If it’s a legitimate need, then that’s what it is.

Get clear on your needs and wants and it’ll help you not only with budgeting on a variable income but in life in general.

Final Thoughts

If your income isn’t set in stone every time you get paid, it can be quite difficult to budget effectively.

But that doesn’t mean it’s impossible.

Use the tips above to get control of your budget even if your money is a little volatile. The key is to do what you can to get the irregularity down.